Strategies in Action

Banning New Fossil Fuel Export Contracts

This page focuses firstly on LNG exports, then coal exports. Banning NEW fossil fuel export contracts is an urgent and relatively easy climate emergency step that could be implemented immediately with almost no adverse economic effects.

Note: This page has not been updated in a while, but unfortunately not much has changed in the last few years, so the key points remain valid.

LNG exports cause massive amounts of avoidable greenhouse gas emissions – emissions which could have been avoided simply by not approving LNG export initiatives over recent years. Existing export contracts might be hard to wind back, but given the climate emergency the Australian Parliament should at least ban any NEW fossil gas and coal export contracts and any NEW offshore oil and gas projects.

Climate impacts of LNG exports

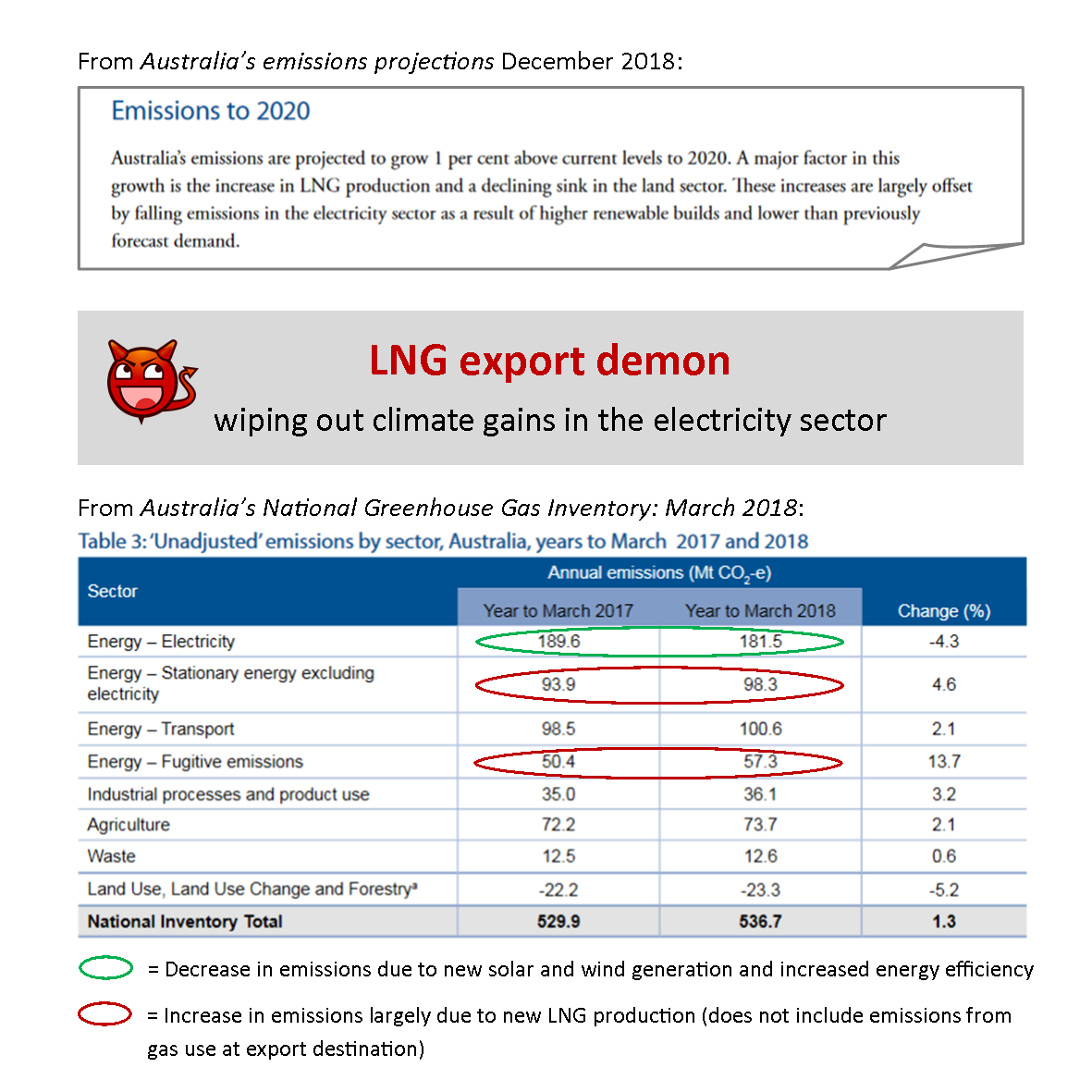

The increase in Australia’s greenhouse gas emissions just from the LNG gas liquefaction process and from associated fugitives, flaring, and venting are greater than the reduction in carbon emissions being achieved by progress on renewable electricity and energy efficiency.

According to Australia’s emissions projections 2018, “Australia’s emissions are projected to grow 1 per cent above current levels to 2020. A major factor in this growth is the increase in LNG production and a declining sink in the land sector. These increases are largely offset by falling emissions in the electricity sector as a result of higher renewable builds and lower than previously forecast demand.”

For example, over the last two years, reservoir gases from Chevron’s Gorgon LNG operations have been vented to the atmosphere instead of being captured and stored, causing the equivalent of about 1% of Australia’s annual national emissions.

The offshore Inpex Ichthys project north-west of Darwin began LNG exports in October 2018. According to The Australia Institute’s November 2018 National Energy Emissions Audit, “The Ichthys gas field consists of two main gas reservoirs, one of which contains 8.5% CO2 in raw gas and the other 17.5% CO2. These are much higher concentrations of CO2 than in any other field supplying LNG projects in Australia, except Gorgon. The Environmental Impact Statement (EIS) for the project estimated that total annual emissions from the project would be about 7 Mt CO2-e, comprising both combustion emissions from the gas consumed to power the liquefaction process, and CO2 stripped from the raw gas prior to liquefaction, and vented to the atmosphere. The 7 Mt will increase Australia’s current annual greenhouse gas emissions by about 1.3%.”

That 7 Mt increase in emissions is just from activities prior to shipping the LNG. When Ichthys is operating at its full capacity of 8.9 Mt/yr, burning that gas at its export destination will produce a further 28.7 Mt/yr of emissions. Shipping and regasification will also add more emissions. In other words, around a quarter of the emissions associated with this LNG project occur before the gas is used for any useful purpose, such as cooking or heating.

But Ichthys is only one LNG project. The total potential output from all 10 LNG export projects in Australia, including Prelude FLNG which is about to commence shipping, is 87.3 Mt/yr (see Appendix A below). The carbon emissions from using that much gas at its destination amount to 282 Mt/yr. To put that in perspective, if Australia’s electricity generation were switched to 100% renewable electricity tomorrow, it would reduce emissions by only 181.5 Mt/yr.

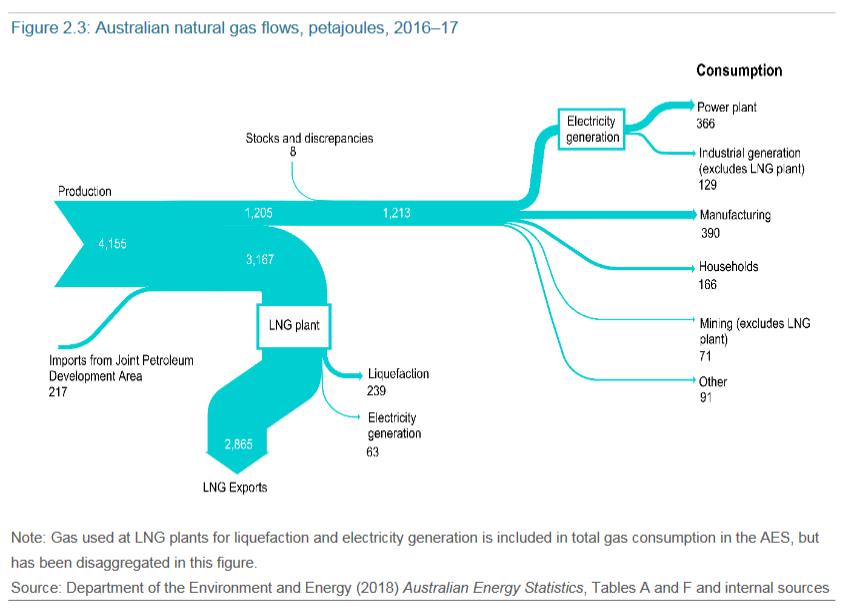

Up to 10% of the gas feedstock is used up during the liquefaction process, and even more gas is used to generate the large amounts of electricity used in the processing. (LNG figures will be higher than shown in the chart below now that the Ichthys LNG project has started operation, and higher still once Prelude FLNG begins full operation.)

The figures below are for LNG in the US, so the transport percentage may differ for Australian LNG exports, but the high percentages of CO2 in the Gorgon and Ichthys raw gas suggests the LNG they export has well over 20% higher climate impact than piped fossil gas.

Of course the CO2 component of the raw gas would still be vented to the atmosphere even if the Gorgon and Ichthys gas were being used domestically and piped to its destination, but all of the Ichthys output for the next 15 years is being exported and most of the Gorgon gas is for export. These projects would never have begun if there were a ban on LNG exports.

The LNG exported from Gladstone is produced mostly from onshore conventional gas and Queensland CSG fields which contain relatively low percentages of CO2 in the raw gas, but even then, liquefaction, fugitive gas, flaring and venting, transport, and regasification add on a lot of extra emissions that achieve no purpose other than enabling export via sea.

Other impacts of LNG exports

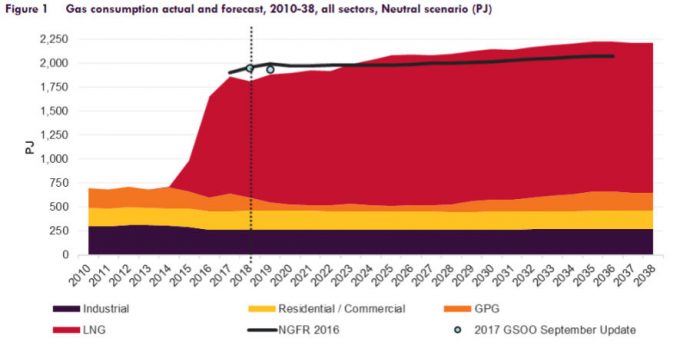

Quite apart from the climate emergency and the extra ‘wasted’ emissions associated with LNG, with the benefit of hindsight it seems crazy that Australia ever allowed LNG exports to commence. Fracking in Queensland has been and continues to be driven primarily by LNG export demand, and LNG exports have caused the price Australian industry and households pay for gas to more than double since Gladstone LNG exports began. Domestic demand for gas is falling and there would have been no reason to lift the fracking moratoriums in WA and NT if it weren’t for LNG export demand.

The Gorgon, Ichthys, and Prelude LNG projects are completely foreign-owned. Ownership by Australian companies is only 16.6% across all 10 current LNG projects. Most LNG companies paid no income tax in 2016-17 despite collectively earning over $70 billion from LNG and other fossil fuel activities in Australia, and only BHP Billiton paid any Petroleum Resource Rent Tax (PRRT) (see Appendix A below). Generally state royalties are not paid on offshore gas extraction (some exceptions in WA), and state royalties add up to only about $1 billion/year Australia-wide for all onshore petroleum royalties (oil + gas).

Not only are we allowing LNG exports to more than wipe out the climate benefit of all our efforts to reduce emissions from the electricity sector, we are also practically giving away the gas and doing so in a way that produces much more climate damage than piped fossil gas.

Click here to share this image on Facebook

But billions of dollars have been invested in LNG facilities on the assumption that Australia will continue to ignore the climate imperative of phasing out fossil fuel use. It is hard to imagine that the Australian government would shut down existing LNG operations, but they could ban any NEW LNG export contracts without missing out on almost any financial benefit. In practice we would probably receive more income tax and PRRT from LNG activities, not less, if any further LNG exports were banned. High levels of investment in new LNG projects count as expenses and will completely offset the tax liability of LNG companies for many years.

Proposals likely to increase LNG export quantities

Plenty of new LNG-related proposals are under discussion and could be stopped simply by banning new LNG export contracts.

Many of the owners of recent new LNG projects off WA and NT are already investing in additional gas supply and planning is underway for even more over the next decade. Chevron is spending $US4 billion to drill 11 extra wells for Gorgon stage two. Inpex was awarded a new exploration area in March 2018 and is planning to add more wells. Shell is planning to bring new gas from the Crux field for processing at the Prelude LNG facilities.

ConocoPhillips is planning new ‘backfill’ wells in its Barossa-Caldita assets in the Bonaparte Basin, located in the Timor Sea, to enable them to continue LNG exports after 2023 when the existing offshore gas supply from Bayu-Undan is expected to be exhausted.

In September 2018 Woodside Petroleum announced that it was proposing to further develop the Browse gas resources by means of a subsea pipeline to the North West Shelf LNG facilities. State and Commonwealth environmental protection authorities have not yet given approval, so it might not be too late to stop this expansion. The three gasfields which would supply this project, Scarborough, Browse and Pluto, contain similar CO2 content to the Ichthys fields.

Even knowing that LNG-related emissions are more than wiping out the climate benefit of efforts to reduce emissions in the electricity sector, the federal government is still allowing and even encouraging yet more fossil gas extraction.

The federal government awarded seven new offshore exploration permits in October 2018:

– Cooper Energy in the Gippsland Basin

– Carnarvon Petroleum Limited in the Timor Sea

– INPEX Browse E&P in the Canning Basin north of Broome

– Shell Australia Pty Ltd in the Timor Sea

– Shell Australia Pty Ltd in the Browse Basin off WA

– Shell Australia Pty Ltd also in the Browse Basin

– BP Development Australia Pty Ltd on the Exmouth Plateau

In December 2018 the federal government announced the successful applicants for Round 1 of Gas Acceleration Program grants totalling $26 million for five new onshore gas projects, four in Queensland and one in the Otway Basin in SA. These grants are specifically for gas intended for the domestic market but would have been completely unnecessary if LNG exports from Gladstone had never been approved. There is no actual gas shortage, just a shortage to meet overseas LNG export contracts as a result of exporters over-estimating the productivity of their at-the-time unproven gas reserves while giving assurances that LNG exports would not lead to domestic shortages. These new projects will simply free up more supply from existing gas wells for LNG exports.

Not incidentally, WA and NT have recently lifted their moratoriums on fracking. WA has more than enough domestic supply due to the overly large take-or-pay contracts already entered into by the WA government. NT gas demand is tiny and could be met for decades just from its current conventional gas source in the Amadeus Basin. Now that the NT fracking moratorium has been lifted, the Northern Pipeline linking NT to the eastern gas network is going ahead and will enable fracked gas from NT to be exported as LNG.

Banning new LNG export contracts would not only stop expansion of offshore gas, it is also highly likely to make it uneconomic to pursue fracking in NT and WA, and possibly even prevent further expansion of fracking in Queensland. Currently 69% of Australian fossil gas is exported, and domestic demand is falling. New gas extraction projects are unlikely if there is a ban on new LNG export contracts.

Coal Exports

Australia is working on reducing emissions from domestic coal use by building new renewable electricity generation and storage, and we need to do that of course, but coal exports have a much greater impact on climate even though the emissions are attributed to the country where it is burnt rather than to Australia. 88% of Australian coal is exported.

When burnt, the 382,788 kt of coal exported in 2016-17 produced around 1,095 Mt of CO2. According to the Quarterly Update of Australia’s National Greenhouse Gas Inventory: March 2018, all electricity generation in Australia currently produces 181.5 Mt/yr of CO2 and Australia’s total emissions are currently 536.7 Mt/yr (less than half the emissions from our coal exports).

SA, NT, and Tasmania already have no coal-fired electricity generation, but the lights would go out in other states if we banned all coal use immediately so nobody is proposing that. However, one thing we can do right now is to ban NEW coal export contracts, and that might well mean we would need no new coal mines to keep the lights on.

According to the Minerals Council of Australia, in 2016-17 coal royalties in the two states that export coal were $3.4 billion for Queensland and $1.6 billion for NSW. A major new hospital costs $1-2 billion. If all coal exports were stopped immediately, Queensland would miss out on around $3 billion in state royalties and NSW would miss out on $1.4 billion. However the ban would apply only to new export contracts so royalty income would diminish only gradually as existing export contracts expire.

Major fossil fuel companies have a high percentage of foreign ownership and many are not good at paying income tax, so banning new coal exports would have much less economic impact than the public is led to believe by industry hype. The following data is from the ATO’s corporate transparency data published in Dec 2018:

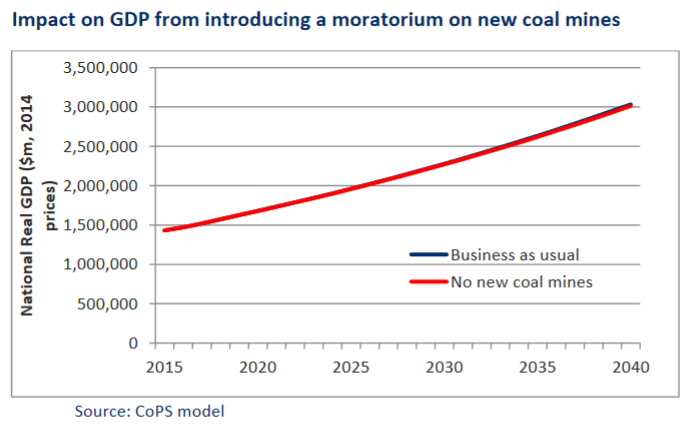

Economic modelling published in Never gonna dig you up! by The Australia Institute and Victoria University’s Centre of Policy Studies (CoPS) shows that the economic impacts of a moratorium on new coal mines or expansions of existing ones — on Queensland, New South Wales and Australia more broadly — would be small.

The coal industry employs less than 0.4% of the Australian workforce and its royalties

contribute just 2% of revenue to the NSW and Queensland budgets. A moratorium on building new coal mines and expanding existing ones would allow for a gradual phase out of the industry, which would in turn minimise the social and economic adjustment associated with worldwide commitments to reduce greenhouse gas emissions.

Australian economic growth is barely affected by a moratorium on new coal mines, with a difference in GDP in 2040 of 0.6% between the two modelled scenarios (“business as usual”, wherein no moratorium is imposed, and a scenario where the moratorium goes ahead.

Conclusions

Most Australian states and territories could relatively easily ban NEW fossil fuel projects for climate reasons under No More Bad Investments (NMBI) legislation (designed to ban new climate-damaging activities in cases where climate-safe options exist). The lights would stay on, the wheels of industry would keep turning, and they’d miss out on very little in economic benefit.

However, as discussed in the States Can analysis paper, existing multi-year export contracts make it difficult for Queensland to ban all new coal mines and gas wells, and for NSW to ban new coal mines, even though otherwise no new coal and gas extraction would be necessary to meet domestic demand.

Stopping new climate-damaging projects before work starts is much simpler than trying to wind back existing projects and set up just transitions for affected workers. State and territory governments can ban new onshore fossil fuel extraction and infrastructure projects but it is the federal government that approves new offshore projects and can control new export contracts.

Oil and gas are often found together, so a federal ban on all new offshore oil and gas projects for climate reasons would stop investment in new offshore LNG export facilities and also prevent sourcing yet more fossil gas to prolong the use of existing LNG facilities. It would also stop drilling for oil in the Bight.

Since WA and NT have just recently lifted their moratoriums on fracking they are unlikely to reverse that decision any time soon, but a federal ban on new LNG export contracts would mean there would be no market for fracked gas from WA and NT.

A federal ban on new coal export contracts would effectively stop coal mining in the Galilee Basin since any new coal mined there would be for export.

These federal bans might sound radical at first glance, but when one considers how much climate damage is caused and how little benefit Australia receives from recent offshore oil and gas projects and current LNG and coal exports, it becomes clear that such bans are not just essential but also a surprisingly effective and easy first step in addressing the climate emergency.

Appendix A: LNG project details